The effects of globalization are best understood in Financial Markets. The Stock Markets are virtually open round the clock, beyond our Indian Market Time of 9.00 AM to 3.30 PM IST. World market start at 6 AM IST when Asian Markets like Japan, China etc opens, SGX opens at 7.30 AM IST, Europe markets open at 1.30 PM IST, US Markets open at 7.30 PM IST and closes at 1.30 AM IST. Since all these markets are interlinked, they demands constant observation.

However, as observed historically, US markets have influenced Indian Markets the most and it attracts attention from all market participants. Every week the US publishes huge macro-economic data, most of which have deep impact on the US equity & commodity Markets as well as other Global Markets.

Since the Great Recession in 2008, US Central Bank (Federal Reserve) has been undertaking series of monetary policy actions to revive the economy. In August 2007, the Federal Open Market Committee”s (FOMC) target for ‘federal funds rate’ was 5.25%. Sixteen months later, with the financial crisis in full swing, the FOMC had lowered the target for the federal funds rate to nearly zero, thereby entering the unfamiliar territory of conducting monetary policy with interest rate at its effective lower bound.

On November 25, 2008, the Federal Reserve announced that it would purchase up to $600 billion in agency mortgage-backed securities (MBS) and agency debt. On December 16, the program was formally launched by the FOMC. On March 18, 2009, the FOMC announced that the program would be expanded by an additional $750 billion in purchases of agency MBS and agency debt and $300 billion in purchases of Treasury securities. This was termed as “Quantitative Easing Phase I (QE1)”.

On November 3, 2010, the Fed announced that it would purchase $600 billion of longer dated treasuries, at a rate of $75 billion per month. That program, popularly known as “QE2”, concluded in June 2011.

On September 13, 2012, the Federal Reserve announced a third round of quantitative easing (QE3). This new round of quantitative easing provided for an open-ended commitment to purchase $40 billion agency mortgage-backed securities per month until the labor market improves “substantially”.

The Federal Open Market Committee voted to expand its quantitative easing program further on December 12, 2012. This round continued to authorize up to $40 billion worth of agency mortgage-backed securities per month and added $45 billion worth of longer-term Treasury securities, thereby making the total bond buying a whopping $85 billion per month.

Riding on the above policy and huge stimulus, the US Markets surged manifold since 2009 but at the same time the entire world got habituated and addicted to the stimulus. Consequently, when Federal Reserve expressed its willingness to scale back the stimulus, markets across the world experienced tremendous shocks. However, FED had no option but to scale back the abnormal Bond-Buying program as their balance sheet had stretched dangerously.

On December 18, 2013 the Federal Reserve Open Market Committee (FOMC) announced they would be tapering back on QE3 at a rate of $10 billion at each meeting. The Federal Reserve ended its monthly asset purchases program (QE3) in October 2014, ten months after it began the tapering process. Markets took a hit initially but gradually digested the tapering over time.

After the end of the QE policies, the entire focus was concentrated on the US Interest Rate (Federal Funds Rate). Quantitative Easing was a liquidity stimulus that was initiated and tapered gradually but the “near zero interest rate” still prevailed and as long as it prevails, liquidity would not be an issue in the markets. Since such ultra-lose monetary policy cannot continue for an indefinite period of time, the new FED Chief Yellen has expressed the necessity to hike interest rates, and as expected the Financial Markets have rejected this idea firmly.

Any issue related to liquidity is of immense importance to emerging markets, especially the Indian Markets. The reason is very obvious. Foreign Investors are the major driving force of the Indian markets and low interest rates across US and Europe is the principal source of their liquidity. Presently, the most important issue to speculate and analyze is the timing of rate hike. Every FOMC meeting is closely watched by the entire world to get a clearer clue as to when the interest rates would be increased. So, any speculation of sooner than anticipated hike in interest rate creates turmoil in the emerging markets and any hint of postponement of rate hike is welcomed. FED will increase the interest rate, although very gradually, but the dreadfully-low inflation and lack of desired growth in the US economy, especially in the job market, are the major hindrances to increasing rates. Therefore, the US macro economic data becomes immensely important for the global markets.

Let us look at the US job data, when and how is it released.

Non-Farm Payroll Data

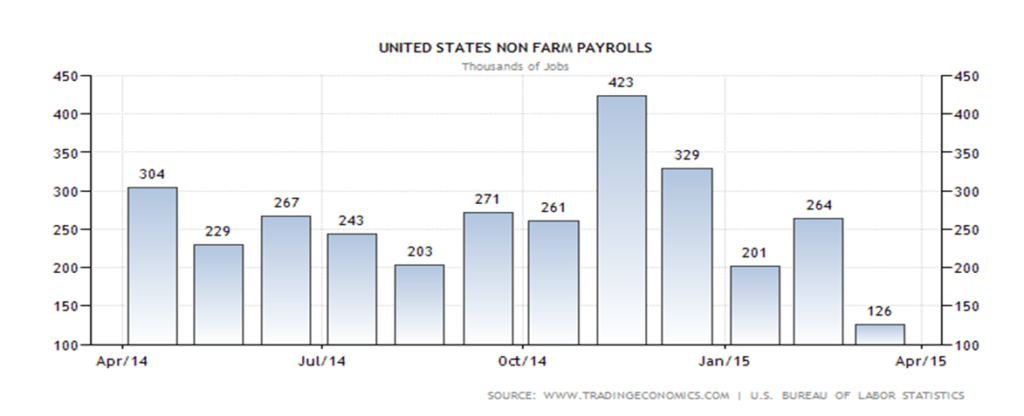

Nonfarm payroll employment is a compiled name for goods, construction and manufacturing companies in the US. It does not include farm workers, private household employees, or non-profit organization employees.

US nonfarm payrolls increased by 126,000 last month, after a downwardly revised 264,000 rise in February, the smallest gain since December of 2013. Meanwhile, the jobless rate remained unchanged at 5.5 percent.

| Source | Bureau of Labor Statistics (latest release) |

| Measures | Change in the number of employed people during the previous month, excluding the farming industry; |

| Usual Effect | Actual > Forecast = Good for currency; |

| Frequency | Released monthly, usually on the first Friday after the month ends; |

| Next Release | May 8, 2015 |

| Impact | This is a vital economic data released shortly after the month ends. The combination of importance and earliness makes for hefty market impacts; |

| Why Traders Care | Job creation is an important leading indicator of consumer spending, which accounts for a majority of overall economic activity; |

| Also Called | Non-Farm Payrolls, NFP, Employment Change |

The overall unemployment rate remains unchanged at 5.5% but last month’s NFP data has been surprisingly poor and further the wage increase remains flat. This data is definitely treated by the FED as a major negative and a hindrance for early rate hike. As a consequence, Dollar weakens and Gold rises.

Apart from all the important monthly NFP data, there are some more job data, vis-a-vis, weekly jobless claim and ADP Payroll data.

Weekly Jobless Claim

| Source | Department of Labor (latest release) |

| Measures | The number of individuals who filed for unemployment insurance for the first time during the past week; |

| Usual Effect | Actual < Forecast = Good for currency; |

| Frequency | Released weekly, 5 days after the week ends; |

| Next Release | Apr 9, 2015 |

| Impact | This is the nation”s earliest economic data. The market impact fluctuates from week to week – there tends to be more focus on the release when traders need to diagnose recent developments, or when the reading is at extremes; |

| Why Traders Care | Although it”s generally viewed as a lagging indicator, the number of unemployed people is an important signal of overall economic health because consumer spending is highly correlated with labor-market conditions. Unemployment is also a major consideration for those steering the country”s monetary policy; |

| Also Called | Jobless Claims, Initial Claims |

In general, poor job data is now good for Emerging Markets and Gold and negative for Dollar. However, reaction of US Markets depends on some more factors. Next week we shall discuss another most important economic data Inflation.

To Be Continued…