Reserve Bank of India’s Monetary Policy is something which is closely watched by every market participant. However often, during RBI announcements, we hear terms which are not common but technical jargons. In order to understand them fully and utilize the opportunities that the announcements present in the Markets, we should recognize what these terms actually mean. Let us discuss few such terms.

Cash Reserve Ratio (CRR)

CRR refers to the fraction of the total Net Demand and Time Liabilities (NDTL) of a Scheduled Commercial Bank, operating in India, that it has to maintain as cash deposit with the Reserve Bank of India (RBI). The requirement applies uniformly to all banks in the country irrespective of an individual bank’s financial situation or size. In contrast, certain countries e.g. China stipulates separate reserve requirements for ‘large’ and ‘small’ banks.

As per the RBI Act 1934, all Scheduled Commercial Banks (that includes public and private sector banks, foreign banks, regional rural banks and co-operative banks) are required to maintain a cash balance, on an average, with RBI on a fortnightly basis to cater to the CRR requirement. Historically, the CRR was mooted as a regulatory tool. However, over the years and especially after the liberalization of the Indian economy in the early 1990s, with the economy experiencing substantial inflows of capital exerting stress on the leverage of the central bank to manipulate liquidity conditions in the domestic money market, the CRR assumed importance as one of the important quantitative tools aiding in liquidity management.

RBI is empowered to vary CRR between 15% and 3%. But as per the suggestion of the Narasimham Committee Report the CRR was reduced from 15% in the 1990 to 5% in 2002. Currently, the CRR is 4%.

The Banks are required to report the CRR compliance to RBI on a fortnightly basis and during the fortnight i.e, on the non-reporting days Banks are required to maintain 99% of their CRR requirement. Earlier this requirement was 70%, however, Mr. Raghuram Rajan, present Governor of RBI, increased this limit from 70% to 99% as additional measure to address exchange market volatility and Rupee slide.

Clearly, CRR is a liquidity tool; a hike in CRR would result in reduction in liquidity and a negative outlook for the Banks and also for the entire markets. On the other hand a cut would result in increase in liquidity, a positive primarily for Banks and also for the entire markets. It should be noted that even if CRR remains unchanged, if the daily requirement of CRR maintenance during non-reporting days is reduced from 99%, the same would have a positive impact on Banks.

Statutory Liquidity Ratio (SLR)

Apart from CRR, every bank in India is required to maintain, at the end of every business day, a minimum proportion of their Net Demand and Time Liabilities as liquid assets in the form of cash, gold and un-encumbered approved securities. The ratio of liquid assets to demand and time liabilities is known as Statutory Liquidity Ratio (SLR). RBI is empowered to increase this ratio up to 40%. An increase in SLR also restricts the bank’s leverage position to pump more money into the economy.

Demand liabilities are those liabilities which are to be repaid at demand (examples: current deposits, savings deposits as per formula, other deposits, inter-bank deposits, etc.). Time liabilities are those liabilities which are to be repaid on expiry of a fixed period (examples: fixed deposits, recurring deposits, etc.).

Now Net Demand & Time Liabilities NDTL = DTL minus a bank”s deposits with other banks. Suppose, a bank has placed deposits of 100 with other banks, and its DTL is 3,000 (including other banks” deposits with it), the NDTL will be: 3,000 – 100 = 2,900.

Both Cash Reserve Ratio (CRR) and SLR are instruments in the hands of RBI to regulate money supply in the economy through banks. SLR restricts the bank’s leverage in pumping more money into the economy whereas CRR is the portion of deposits that the banks maintain with the Central Bank to reduce liquidity in banking system. Thus, CRR controls liquidity in banking system while SLR regulates credit growth in the country.

The other difference is that to meet SLR, banks can use cash, gold or approved securities whereas to maintain CRR it has to be only cash. CRR is also used to control inflation.

Presently SLR is 21.5%, last revised on 3rd February 2015 from 22%, which was continuing since 9th August 2014.

Repo and Reverse Repo

These are the key interest rates. Repo rate is the rate at which RBI lends to commercial banks usually against government securities. Reduction in Repo rate helps the commercial banks to borrow money at a cheaper rate and increase in Repo rate makes it expensive for commercial banks to borrow money from RBI.

Reverse Repo rate is the rate at which RBI borrows money from the commercial banks.

An increase in the Repo rate will increase the cost of borrowing and lending of the banks which will discourage the public to borrow money and will encourage them to deposit. As the rates are high the availability of credit and demand decreases resulting to decrease in inflation. This increase in Repo Rate and Reverse Repo Rate is a technique to tighten the monetary policy.

An increase in Repo Rate has negative impact primarily on Banks and other sectors which are affected by cost of bank loan like Auto, Housing etc. A reduction has an opposite impact.

In India, interest rate decisions are taken by Reserve Bank of India”s Central Board of Directors. The official interest rate is the benchmark repurchase rate. In 2014, the primary objective of RBI’s monetary policy became price stability, giving less importance to government”s borrowing, stability of the rupee exchange rate and the need to protect exports. In February 2015, the government and the central bank agreed to set a consumer inflation target of 4%, with a band of plus or minus 2 percentage points, from the financial year ending in March 2017.

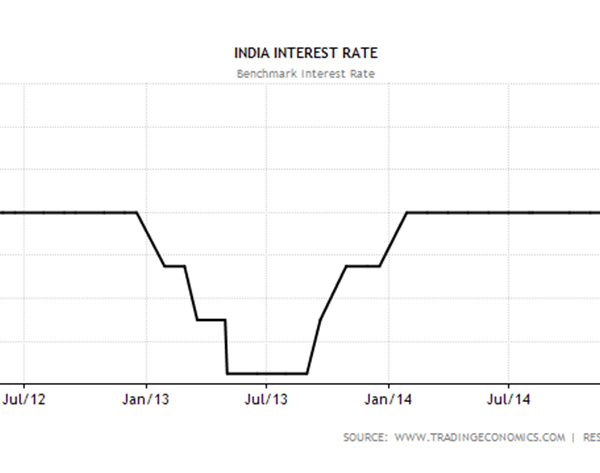

The above graph shows key interest rates were hiked after June 2013 and remained unchanged for a long period and were reduced slightly after December 2014. Overall the interest rate is still on the higher side, since RBI is still not convinced that inflation can sustain at lower level. Industries and Government have urged to cut the interest rate, in order to fuel growth of the economy. The latest deep decline in both CPI and WPI could make the RBI reconsider the rates soon.

Marginal Standing Facility (MSF)

MSF came into effect from 9th May 2011. MSF scheme is provided by RBI through which banks can borrow overnight up to 1% of their net demand and time liabilities (NDTL). However, with effect from 17th April 2012 RBI has raised the borrowing limit under the MSF from 1% to 2% of their NDTL outstanding at the end of the second preceding fortnight. The rate of interest for the amount borrowed through this facility is fixed at 100 basis points (i.e. 1%) above the repo rate for all scheduled commercial banks. However, the rate of interest on the amount borrowed from this facility got fixed at 300 basis points (i.e. 3%) above the repo rate with effect from 15th July 2013. In addition, access to the LAF window was reduced by RBI to just 0.5% of their NDTL which in turn forced banks to access the MSF window for their requirements. In the credit policy of September 2013, this was reversed, whereby MSF rate was cut by 75 bps from 10.25% to 9.5% and as on September 2013 MSF stands at 200 bps (2%) above the repo rate, which is considered as the “policy rate” in the economy.